Paper trading can teach the workflow. Live execution tests whether that workflow survives real fills, real delays, and real account pressure. The candle may look the same. The trade path will not.

That is the core difference. A trade does not become real on the chart. It becomes real when the order is submitted, acknowledged, filled, partially filled, adjusted, or canceled in a live market. Paper may show a smooth path from signal to entry to exit. Live trading adds the parts that are harder to model: spread, liquidity, latency, partial fills, and the trader’s own reaction when real capital is involved.

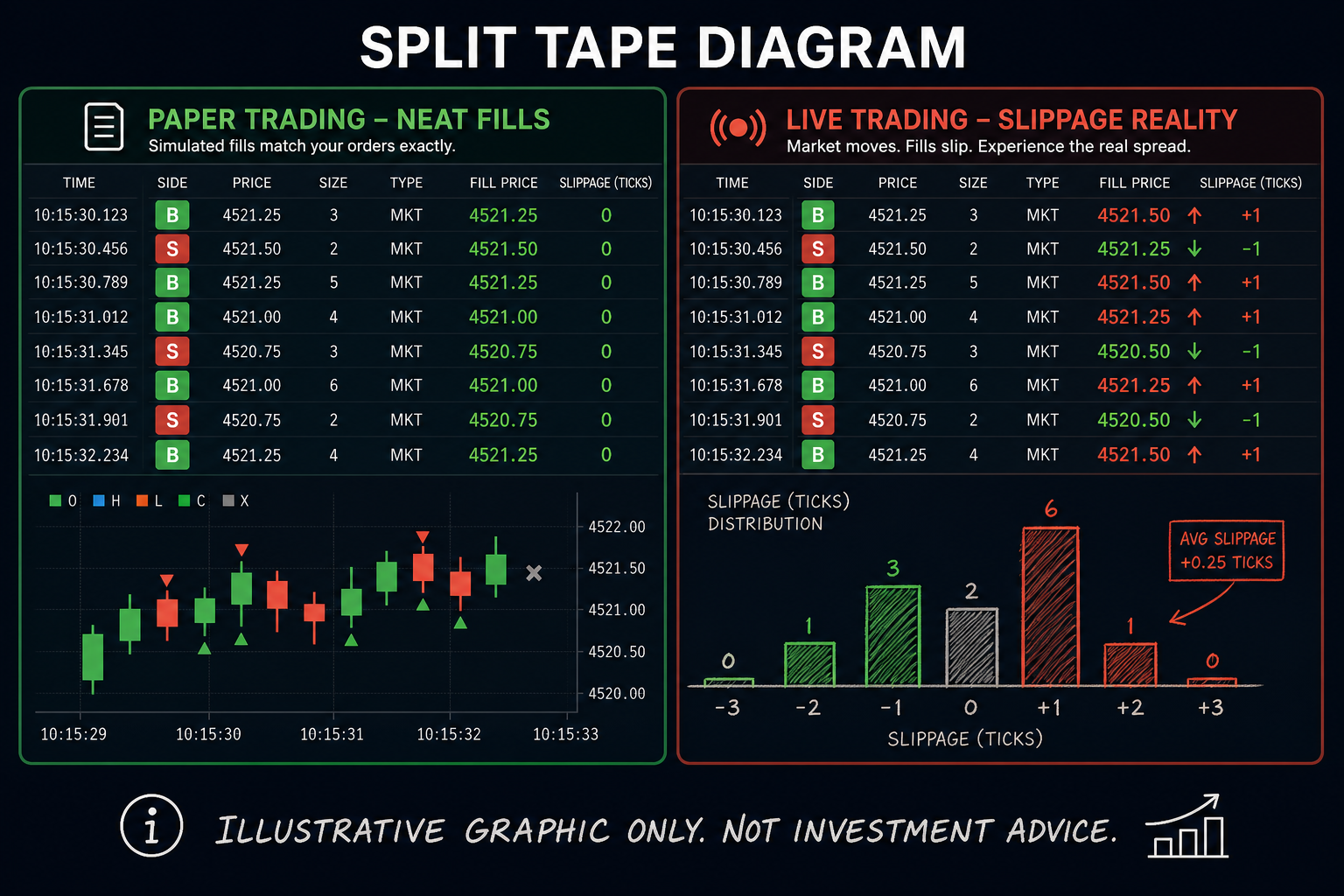

Slippage and latency are not side issues. They can change entry quality, bracket spacing, stop distance, partial exit behavior, automation timing, and whether a repeated setup still makes sense under live conditions.

OHLCX is built around that execution layer. The platform helps traders express their own plan through structured order logic, with live execution, exit flows, risk visibility, and optional automation supporting the workflow without replacing judgment. Capital and custody stay with Schwab. The trader’s decisions stay with the trader.

Paper trading is practice, not proof

Paper trading is useful because it lets traders rehearse the mechanics before money is involved. It can help with order fields, entry sequence, OCO or OTOCO layouts, bracket structure, partial exit planning, and the basic rhythm of a workflow. A trader who cannot operate the order form calmly in paper will not usually operate it better when the position is live.

But paper trading should not be treated as proof that a setup will behave the same way in the market.

A simulated fill does not carry the same friction as a live fill. It does not reflect the spread at the moment the order reaches the market, or the partial fill path that leaves the trader managing less size than planned. It also does not show how the trader will react when the fill is worse than expected and the account balance is real. Paper can rehearse the order path. It cannot prove the live path.

When a fill changes the rest of the trade

The first break between paper and live is usually not the idea. It is what the fill does to everything attached to it. A partial fill can leave the trader with less size than planned while the bracket or exit logic was built around a full position. A worse entry can make the original stop too wide for the intended risk. A delayed fill can make the first target less attractive. A limit order that never fills can leave the trader chasing or canceling instead of following the plan.

The problem is not only that the fill is different. The problem is that everything attached to the fill may need to be checked and reset before the trade is still valid. The trader has to confirm what filled, what remains open, whether the stop still matches the live position, and whether attached exits still reflect the actual size. If that review does not happen, the order can look structured on screen while the real risk has already shifted.

This is where paper trading hides work. In paper, the position moves neatly from planned entry to planned exit. In live execution, the trader may be managing partial size, a different average price, a wider spread, or a bracket that no longer fits what is actually in the account.

What slippage actually changes

Slippage changes more than the entry price. A worse fill can change the entire risk profile of the trade. It can make the stop feel too close, the target less worth holding for, or the planned partial exit less meaningful. If the trade was designed around one entry and the trader gets filled somewhere worse, the rest of the order may no longer make sense at its current levels.

This matters even more for repeatable workflows. A setup that works cleanly on paper may depend on fill quality that simply does not exist during the open, around news, or in a name with a wide spread. If the live path is consistently worse than the paper path, the problem is usually not the idea. It is the execution assumption underneath it.

Here is what that looks like in practice. A trader notices their morning entries are consistently getting filled ten to fifteen cents worse than their paper results. That is not a signal problem. That is a timing problem. The fix is either moving entries to a calmer session window or widening the acceptance band so the strategy is not depending on fills it cannot reliably get.

The same logic applies to automation. A Strategy Builder path or no-code automation template built around clean paper assumptions still needs to be tested against live conditions. A repeated workflow only stays useful if its timing, spacing, and exit logic still hold up once real fills are part of the result.

Tracking slippage does not need to be complicated. A trader can note the session phase, order type, liquidity conditions, and whether the trade was manual or automated. The goal is not a perfect model. The goal is to see whether the assumptions the trader is making are too optimistic for the way the trade is actually being executed in the market.

Psychological slippage is real too

Not all slippage is in the fill. A trader can slip from the plan after the order is live. A worse-than-expected entry may lead to widening the stop to avoid being proven wrong. A partial fill may create hesitation about whether to add size or wait. A fast move may cause the trader to trim earlier than the plan called for. A loss earlier in the session may lead to smaller size on a valid setup or larger size on a trade that is really about recovering what was lost.

That is psychological slippage. The trade starts with a written plan, but the live experience changes the trader’s behavior. This is why paper trading can feel controlled while live trading feels different. In paper, there is no real account balance reacting to each decision. There is no same-day regret after a bad fill. There is no pressure to fix a trade because the entry was not perfect.

A workflow should make those moments easier to manage. One useful guardrail is to define the review point before the trade is live: no stop changes, size changes, or early exits unless the original invalidation is hit or the market condition has clearly changed.

If the fill does not invalidate the plan, the trade should not be rewritten just because the entry feels uncomfortable. If the trader is repeatedly editing stops, changing size, or exiting early after live friction appears, that is not only a discipline problem. It is execution data. The workflow may need different entry spacing, a cleaner review point before any adjustment is allowed, or a stricter rule about when a trade is still worth managing versus when it should simply be closed.

Compare the planned path to the live path

The most useful review starts with one question: did the trader adjust the trade because of the market, or because of discomfort? That question separates execution reality from emotional reaction. From there, a practical review can ask:

- What entry was planned and what fill was actually received?

- Was the full size filled or only part of it, and did the bracket still match?

- Did slippage change the risk profile enough to warrant reviewing the attached orders?

- Did automation behave as expected under live conditions?

- Did the trader change the plan because conditions changed, or because the live trade felt uncomfortable?

These questions help separate a setup problem from an execution problem. If the idea was reasonable but fills were consistently poor, the issue is likely timing, order type, or session choice. If fills were acceptable but the trader kept editing the plan, the issue is behavioral. If partial fills repeatedly left the position hard to manage, the workflow needs clearer rules for what happens to remainders. Live execution review turns the gap between paper and live into something the trader can actually close over time.

Build workflows that expect friction

The goal is not to make live trading feel like paper. It will not. The better goal is to build workflows that expect friction. That means planning for slippage, checking acknowledged fills, reviewing remaining size after partials, and making sure attached orders still match the position that is actually live.

It also means being honest about when a repeated setup needs to be adjusted. If live fills are consistently worse near the open, the trader needs different timing or wider acceptance bands. If thin liquidity keeps turning staged exits into poor fills, the exit plan needs to be simpler. If automation adds orders faster than the trader can verify them, the workflow needs a tighter boundary.

OHLCX supports this kind of execution-first process by helping traders work from structured order logic instead of relying on memory once the trade is live. It gives traders a way to define order logic, manage exits, and keep more of the execution workflow visible as the trade moves from plan to live order.

Paper can rehearse the order. Live execution proves whether the order can survive the market. To see the workflow in action, request a walkthrough through the OHLCX platform page.

Leave a Reply